Regularly checking in on your business is essential to keep it moving in the right direction. One of the key areas to look at is inventory management.

How has inventory management been working for your small business? Have you had the right products available when needed? Did you miss out on sales because items were out of stock? Or, did you end up losing money because of too much stock?

In this article, we’ll cover some basic inventory management techniques, what to look for in quality inventory software, and share best practices to help you manage your inventory more effectively.

What is Inventory Management?

Inventory management is about making sure you have the right products in the right amounts, ready to sell when customers want them. When done well, it helps keep costs down by avoiding excess stock, while also boosting sales. With good inventory management, you can track stock in real time, making the whole process smoother.

Managing inventory effectively means you’re less likely to run out of popular items or have cash tied up in too much stock. It also helps make sure products are sold before they spoil, become outdated, or take up unnecessary space in your storage.

Good Inventory Management Software should:

- Cut costs, improve cash flow, and boost your profits

- Track your inventory in real-time

- Help you predict demand more accurately

- Avoid product shortages and production delays

- Prevent having too much stock or too many raw materials

- Make inventory analysis easy on any device

- Access it directly from your retail point-of-sale

- Organize your warehouse efficiently, saving employee time

- Speed up intake with quick barcode scanning

- Manage inventory across multiple locations or warehouses effortlessly

Inventory Management Techniques and Best Practices for Small Business

Here are some techniques small businesses often use to manage inventory:

- Fine-tune your forecasting. Accurate forecasting is key. Use past sales data, market trends, growth predictions, and planned promotions to help you estimate future sales. If you’re using Square, you can find historical sales info in your Dashboard.

- Use the FIFO method (first in, first out). Sell goods in the same order you bought or created them, especially for perishables like food or makeup. FIFO also works well for non-perishable items to avoid damage or expiration. To apply FIFO, store new stock in the back so older items are easier to access.

- Identify slow-moving stock. If certain items haven’t sold in six to twelve months, it might be time to stop stocking them. You could also try a discount or promotion to clear them out, as excess stock takes up valuable space and capital.

- Audit your stock. Even with inventory software, periodic physical counts are essential to make sure stock records match reality. You can do a full count once a year or spot-check fast-moving items more frequently.

- Use cloud-based inventory software. Look for software that offers real-time analytics. For example, Square’s system connects to your point of sale and updates stock levels with each sale. You can also set up daily stock alerts to reorder items before they run out.

- Track stock levels constantly. Have a reliable system for tracking inventory, especially for high-value items. Good software can handle much of this, saving time and reducing costs.

- Reduce equipment repair delays. Keep track of essential machinery and its parts so you’re prepared for repairs before issues arise. Unexpected breakdowns can be costly.

- Maintain quality control. Regularly check that products are in good shape and correctly labeled. Quick inspections during stock audits can help catch any problems early.

- Consider a stock controller. If you have a large inventory, hiring a dedicated person to handle purchase orders, deliveries, and inventory checks can be a smart move.

- Use the ABC method. Many businesses categorize inventory by value:

- A items are high-value products with lower stock numbers.

- B items fall in the middle.

- C items are lower-cost items that make up the bulk of inventory.

- Think about drop shipping. With drop shipping, you can sell products without keeping them in stock. Instead, a wholesaler or manufacturer handles storage and shipping, freeing up your space and resources. This approach is common in online stores but can work for any business model.

The chart below, based on Lokad’s recommendations, breaks down how to classify A, B, and C items by annual consumption value.

| ABC Inventory Analysis Example | ||

|---|---|---|

| Classification | Percentage of inventory | Annual consumption value |

| A | 10-20% | 70-80% |

| B | 30% | 15-25% |

| C | 50% | 5% |

Square for Retail

A point of sale inventory system built for small business

Square’s retail POS includes powerful inventory management that updates in real time, so you can keep track of stock from anywhere. Perfect for omnichannel retail, it syncs easily with both your physical store and online shop.

Our inventory system is quick to set up and simple to use. You can download reports and get daily stock alerts for items running low or out of stock, keeping you in control at all times. Find out more about its use here.

For multi-channel inventory management, Square POS easily interfaces with programs like Stitch Labs, Shopventory, and DEAR if you require a more sophisticated solution. You can also work with a developer to build a custom solution using the Square Items API. With flexible options, Square makes it easy to switch your POS system, keeping your business running smoothly and your inventory flowing.

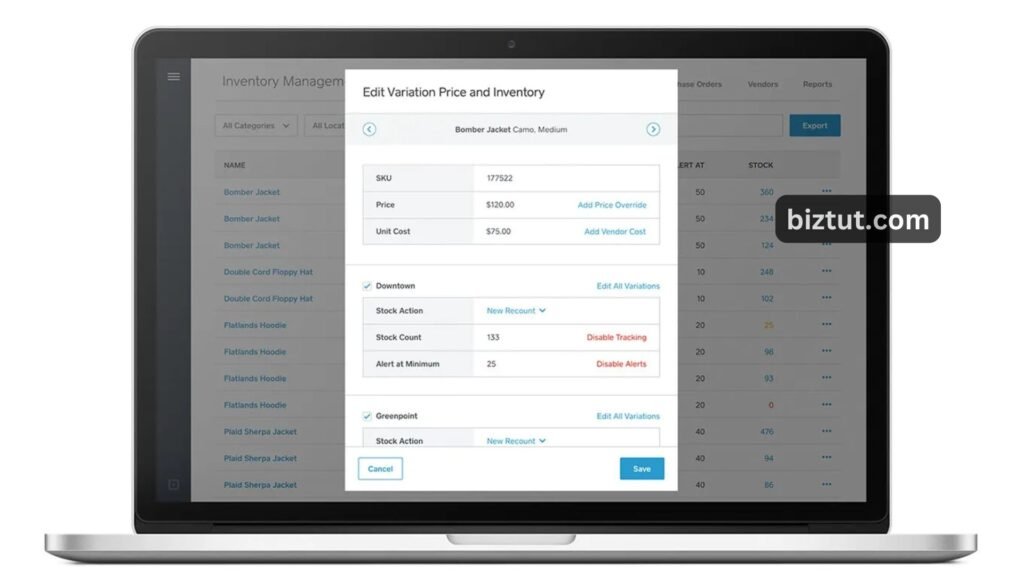

How to track and manage inventory with Square

Square’s free cloud-based inventory management software makes it easy to track stock by item or in bulk. When you enable inventory tracking, stock levels automatically update with every sale made through the Square app, Square Invoices, or your online store. You can manage inventory per location, even using SKUs if needed.

How to Track Inventory by Item:

- Navigate to your Dashboard’s Item Library.

- Select the item you want to track.

- Adjust the item count and choose the location (inventory can be set, edited, and tracked for each location separately).

Once tracking is set up, you’ll get alerts in your Dashboard when items are low or sold out, so you’ll know when to reorder and restock.

How to bulk upload inventory

Got a lot of items to update? No problem! You can download a report of your current inventory and use the import tool to make bulk updates. This is perfect for adding new stock or double-checking what you already have.

Just follow these steps:

- Open your Dashboard and navigate to the Item Library.

- Click “Modify Item Library.”

- Download the template file (this will include your full item list).

- Open the file and add your inventory numbers in the “New Quantity [Location]” column.

- You can also set stock alerts in the “Stock Alert Enabled [Location]” column.

- Drag and drop the file into the Import Inventory box after saving it, then select “Upload.”

And you’re done!

Tips for businesses who make their own products

Some businesses control their entire supply chain—like a company that makes and sells handmade messenger bags. Instead of buying finished products, they source raw materials and create the products themselves. These types of businesses often have three main inventory types:

- Raw materials used to make products

- Work-in-progress pieces

- Finished products

Managing inventory well is crucial, as shown by Cisco’s mistake in 2001. When they overestimated demand, they had to write off $2.25 billion in raw materials and components—a costly result of poor inventory planning and inaccurate sales forecasting.

Tips for Retail Businesses

Even if you’re not a large corporation, smart inventory management can save you a lot of money. It might seem tempting to buy large quantities to get vendor discounts or free shipping, but too much stock can hurt your business. Having excess inventory ties up funds and risks a loss if items don’t sell on time. This is especially tricky with seasonal items; for instance, after Christmas, consumers expect discounts on holiday items, which can mean selling at a loss.

Conversely, a shortage of inventory may result in lost sales. If customers come in and find their favorite item is out of stock, they’re likely to shop elsewhere. A study by GT Nexus found that 63% of German shoppers who encountered an out-of-stock item bought it from a competitor or skipped the purchase altogether.

Also Read: How to Create a Business Workflow?

Handling Lost, Damaged, or Stolen Items

Inventory loss, known as shrinkage, is a common problem for retailers. In 2016, shrinkage cost retailers over $49 million, and the average rate is about 2%. Shrinkage comes from several sources:

- Shoplifting: 38%

- Employee theft: 34.5%

- Paperwork errors: 16%

- Supplier/vendor fraud: 7%

- Unknown causes: 6%

Damaged goods are also part of shrinkage, whether they get damaged on their way to the store or in-store.

Shrinkage hurts profits, as it’s a double loss—you lose the cost of the item and the revenue you’d make from selling it. Some retailers raise prices to cover these losses, but that can push customers away if they’re price-sensitive. You might also consider extra security measures, but that increases costs.

While shrinkage is part of retail, you don’t have to treat it as a total loss. Talk to your tax advisor to see if you can deduct inventory-related losses, like theft or damage, on your taxes.